When you retire from military or federal service, your TSP balance is one of the larger financial assets you’ll manage in retirement. Many retirees keep TSP exactly as-is for years — and for most, that’s the right choice. But there’s a real decision to make: keep it in TSP, roll it over to an IRA, or convert part of it to a TSP annuity. Each option has tax implications, flexibility tradeoffs, and downstream consequences that compound over decades.

Here’s the framework I’ve used to talk retiring service members through this decision.

Option 1 — Keep It in TSP

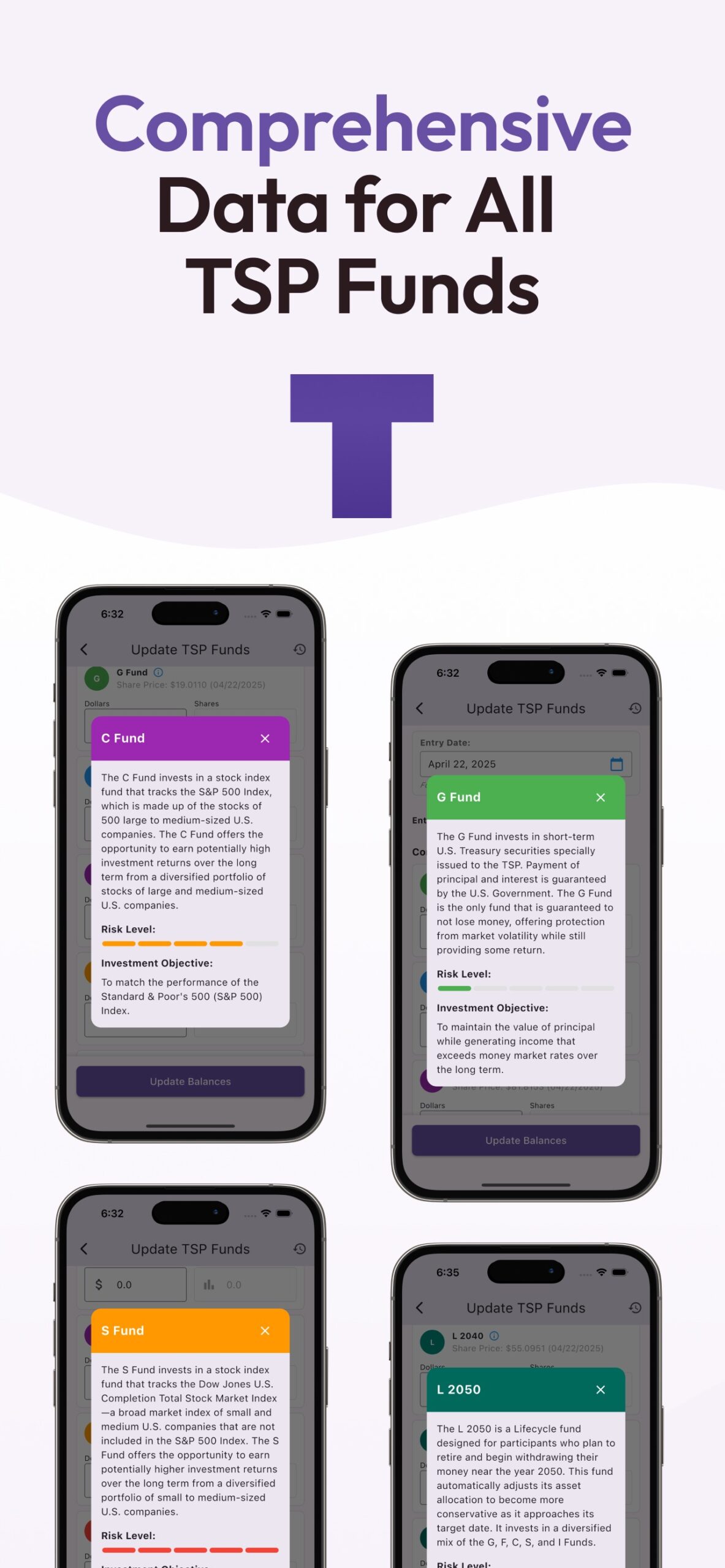

The default option. After retirement, your TSP balance stays in the plan. You can continue to allocate among G/F/C/S/I and Lifecycle funds. You can withdraw partial amounts as needed or take regular monthly distributions.

What you keep:

- The lowest expense ratios in the industry (TSP funds run at roughly 0.05% expense vs. 0.10-0.50% typical for retail mutual funds)

- Institutional-quality fund management

- Familiar interface and tools

- Spousal beneficiary protections built in

What you give up:

- Some flexibility in withdrawal mechanics (TSP withdrawal rules are simpler than IRA but less granular)

- Limited fund selection (G/F/C/S/I and L funds vs. hundreds of options in a brokerage IRA)

- Some estate planning complexity (TSP beneficiary rules differ from IRA)

For most retirees, keeping at least the majority of the balance in TSP is the right call. The expense advantage compounds across 20-30 years of retirement. A 0.5% annual expense difference between TSP and a typical retail brokerage on a $400K balance is $2,000/year — over 25 years, with compounding, that’s roughly $80,000 of foregone returns.

Option 2 — Roll Over to an IRA

You can roll your TSP balance into a Traditional IRA (or Roth IRA if your TSP is Roth) without triggering current-year taxes. This gives you broader investment options and more flexibility, at the cost of higher expenses.

Reasons retirees roll over:

1. Specific investment access. If you want to invest in REITs, individual stocks, sector funds, or alternatives, you need a brokerage account. TSP doesn’t offer these.

2. Consolidation. If you have multiple retirement accounts (TSP, prior employer 401k, personal IRA), consolidating into one IRA simplifies portfolio management. A single account, single allocation, single withdrawal strategy.

3. Estate planning. IRAs offer more granular beneficiary controls. TSP has a sequential beneficiary system; IRAs allow customized beneficiary designations with trusts, percentages, and contingent beneficiaries.

4. Roth conversions. Converting Traditional to Roth requires the account to be in an IRA or 401k that allows conversions. TSP’s Roth conversion rules are more restrictive than IRA’s.

Reasons NOT to roll over:

- The expense ratio difference (described above) is meaningful over decades

- You need the discipline of fewer options — too many choices leads to over-trading

- TSP’s fund quality is competitive with the best institutional alternatives

Option 3 — TSP Annuity

You can convert part or all of your TSP balance into a lifetime annuity through MetLife (TSP’s contracted annuity provider). The annuity pays a fixed monthly amount for the rest of your life (or your and your spouse’s life if joint).

The math: annuity rates depend on your age, interest rates at conversion, and whether you elect a survivor benefit. At current rates, a 65-year-old converting $200,000 to a single-life annuity might receive $14,000-$16,000/year for life ($1,167-$1,333/month).

Reasons to consider annuity:

- Longevity protection. If you live to 95, the annuity has paid you for 30 years from a single purchase.

- Removes withdrawal decisions. No need to manage drawdown rate.

- Useful for retirees worried about outliving their savings.

Reasons against:

- Annuity rates are typically conservative — you’d usually do better self-managing a portfolio with a 4% withdrawal rate

- Annuity payments don’t fully adjust for inflation

- The annuity money is gone — your heirs don’t inherit it (unless joint with survivor benefit, which lowers the payment)

- Irrevocable. Once converted, you can’t get the balance back.

For most retirees, the annuity makes sense for a small portion of the balance (say 25-30%) as longevity insurance, while keeping the rest invested for growth and flexibility.

Withdrawal Mechanics After Retirement

If you keep TSP, you’ll eventually start withdrawing. The mechanics:

Required Minimum Distributions (RMDs). Starting at age 73 (under current law), you must withdraw a minimum amount each year. The percentage is set by IRS tables and increases with age. Skip an RMD and you face a 25% penalty on the missed amount.

Substantially Equal Periodic Payments (SEPP). If you retire before 59.5, you can take SEPP withdrawals without the 10% early-withdrawal penalty. Once started, the schedule must continue for 5 years or until 59.5, whichever is later.

Partial and lump-sum withdrawals. TSP allows partial withdrawals at any time after retirement. Most retirees use this for ad-hoc needs while leaving the bulk invested.

Monthly distributions. You can set up automatic monthly payments at a specified rate. Useful for replacing employment income without manual withdrawals each month.

The Tax Question

Withdrawals from Traditional TSP are taxed as ordinary income at your then-current marginal rate. Roth TSP withdrawals are tax-free if you’re 59.5+ and the account is 5+ years old.

For most military and federal retirees, post-retirement marginal tax rate is similar to or slightly lower than peak-career marginal rate. The Roth-vs-Traditional decision made during career affects how withdrawals are taxed in retirement.

One advantage of TSP in retirement: simpler tax reporting than IRA aggregation rules. TSP issues a single 1099-R for total annual withdrawals. Multiple IRAs require careful tracking of per-account basis and pro-rata distribution rules.

The 4% Rule and Modern Variants

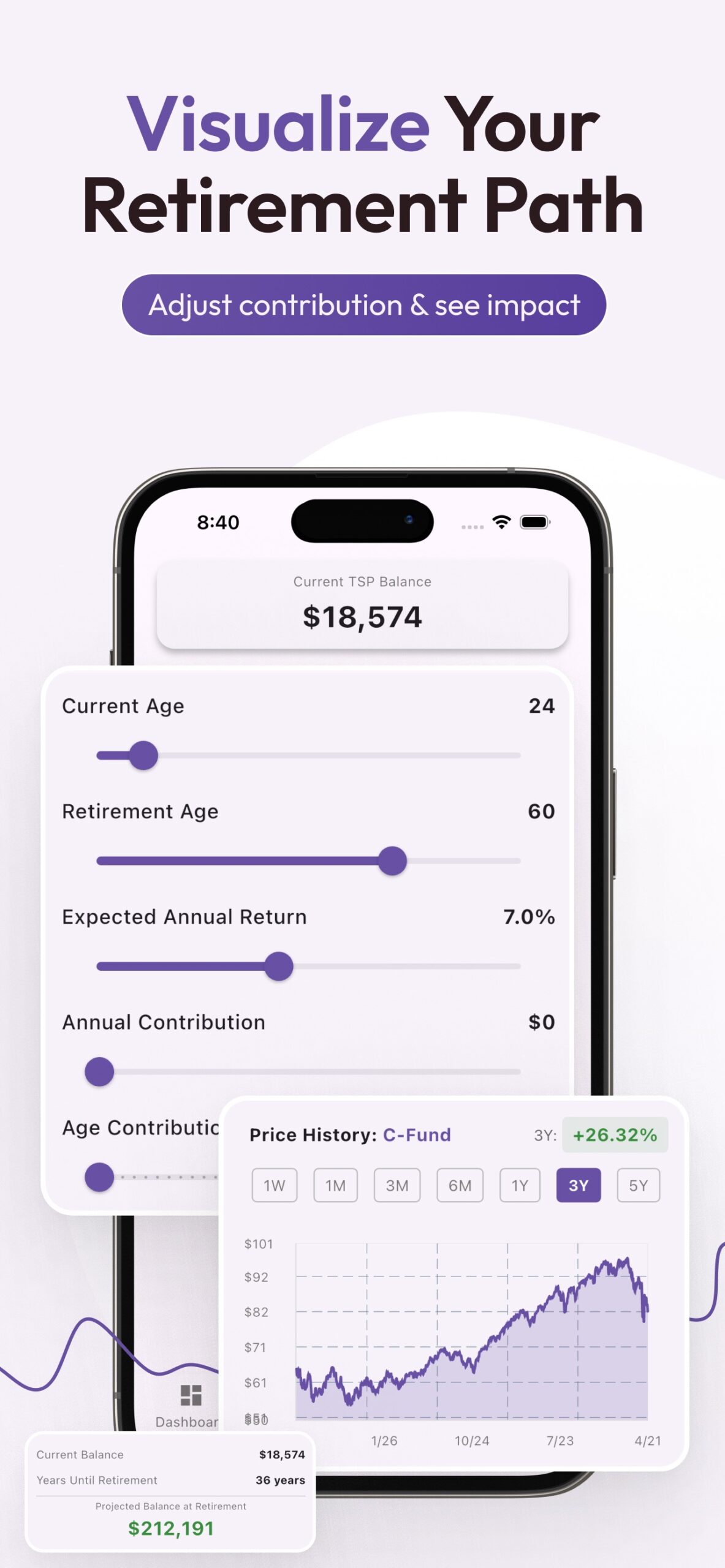

The classic retirement withdrawal rule: take 4% of your starting balance in year one, increase each subsequent year by inflation. This rule was based on historical market returns and shows roughly 30 years of sustainability across various market scenarios.

For a $400,000 TSP balance, 4% = $16,000/year ($1,333/month) initial withdrawal. Adjusted upward each year by CPI.

Recent updates to the rule:

- 4.0% is still the baseline conservative rate

- 3.5% is “safer” for retirements expected to exceed 35 years

- 4.5-5.0% is “aggressive” — possibly sustainable but with more sequence-of-returns risk

- Variable spending rules (e.g., “spend more when market is up, less when down”) can support higher rates

Most retirees end up at 3.5-4% as a default. The TSP balance is one of typically several income sources — military pension, VA disability, Social Security, possibly civilian career savings — so the withdrawal rate matters less when other sources cover baseline expenses.

The Mistake Many Retirees Make

The single most common TSP mistake among retirees: rolling everything to a brokerage IRA without doing the cost comparison. The broker-dealer or financial advisor recommending the rollover earns fees on the rollover (asset-based fees on the IRA balance); the retiree pays higher expenses indefinitely.

Before rolling over, calculate:

- TSP expense ratio vs. proposed IRA expense ratio

- Advisor fees if using a managed account

- Trading costs if self-managing

- Total annual cost as % of balance

If the total cost exceeds 0.5% per year vs. TSP’s ~0.05%, you’re giving up significant compound returns. Multiply that 0.45% difference by your balance, then by 25 years, then add the lost compounding — the number is large.

The Optimal Strategy for Most Retirees

Based on what works across many retirement profiles:

1. Keep at least 50-70% of the balance in TSP. The cost advantage is real and compounds.

2. Roll over 20-30% to an IRA if you need investment flexibility. Use this for specific assets (REITs, individual stocks) or for Roth conversion strategy.

3. Consider annuitizing 20-25% only if longevity risk concerns you. Most retirees skip the annuity entirely; that’s also fine.

4. Don’t make any decisions immediately at retirement. The TSP balance can sit unchanged for months or years. Take time to evaluate; the choice is reversible (except annuity, which isn’t).

For the related discussion of TSP fund allocation by career stage, see the TSP fund allocation by age breakdown.

Stay in the loop

Get the latest dod retire.com updates delivered to your inbox.