For military retirees who transition to federal civilian employment under FERS — and for the substantial population of military spouses, veterans, and dual-status careers who work both sides — the federal retirement calculation is its own animal. FERS combines a defined-benefit pension, TSP with matching, and Social Security into a three-legged stool. Layered on top is the military buyback decision: federal employees with prior military service can buy back those years to count toward FERS pension, often producing a substantially higher monthly retirement payment.

The math gets complicated quickly. Here’s how FERS calculates in 2026 and why military-experienced federal employees should treat the buyback question as a top-priority decision.

The FERS Pension Formula

Under standard FERS, the monthly annuity is calculated as:

Annual Annuity = 1.0% × Years of Service × High-3 Average Salary

For an employee retiring with 25 years of FERS service and a high-3 average of $120,000, that’s $30,000/year or $2,500/month.

Two enhancements modify the basic formula:

1.1% multiplier for late retirees. If you retire at age 62 or later with at least 20 years of service, the multiplier is 1.1% instead of 1.0%. The same 25-year, $120,000 high-3 employee retiring at 62 instead of 60 gets $33,000/year. The 10% boost is worth pushing to 62 if you can.

Military buyback. Federal employees with prior military service can buy back those years to count toward FERS service. The cost is approximately 3% of military base pay during those years (plus interest if more than 2 years post-separation when paying). The benefit is years of additional FERS service. Discussed below.

Minimum Retirement Age (MRA)

FERS has an MRA structure that determines when you can retire with full benefits:

| Birth Year | MRA |

|---|---|

| Before 1948 | 55 |

| 1948-1952 | 55 + 2 months per year after 1947 |

| 1953-1964 | 56 |

| 1965-1969 | 56 + 2 months per year after 1964 |

| 1970 or later | 57 |

At MRA with 30+ years of service, you can retire with full immediate annuity. At MRA with 10-30 years, you can take a reduced annuity (the “MRA+10” option). At 62 with 5+ years, full immediate annuity. At 60 with 20+ years, full immediate annuity.

Military Buyback — The Highest-ROI Decision

For federal employees with prior military service, buying back military time to count toward FERS pension is often the single highest-ROI financial decision of their federal career.

How it works:

- Calculate the deposit owed (approximately 3% of basic military pay during service years, plus accrued interest if paying after 2-year window)

- Pay the deposit (lump sum or installment plan)

- The military years count toward your FERS service for both annuity calculation and retirement eligibility

Concrete example: an Army E-5 with 8 years of service who transitions to civilian federal at GS-11. After 22 years of federal civilian service, they’re at 30 years of total service for FERS purposes (8 military + 22 federal). The high-3 for FERS uses civilian salary only (military pay doesn’t count toward high-3).

The math for buyback ROI:

- Buyback deposit cost: roughly $7,000-$15,000 for 8 years of military service (depending on rank/pay)

- Pension benefit at retirement: 8 additional years × 1.0% × high-3 (say $140,000 at 62) = $11,200/year additional

- Over a 25-year retirement, that’s $280,000+ in additional pension payments

- ROI ratio: roughly 20-40x

The buyback also helps you reach 30 years of service earlier, which qualifies you for the MRA+30 immediate annuity option. For many federal employees, the buyback is what makes early retirement possible.

Catch: military years that already provide a military retirement pension can’t be double-counted for federal pension. If you retired from military service and receive a military pension, you generally can’t buy back those years for FERS unless you waive the military retirement pension (which usually doesn’t make sense). Active military service that didn’t result in a 20-year retirement is buy-back eligible.

The FERS Supplement — Bridge to Social Security

FERS employees who retire before age 62 with eligibility for immediate retirement receive a FERS Annuity Supplement until age 62. The supplement approximates the Social Security benefit you would receive at 62 based on your federal service.

For someone retiring at 60 with 30 years of FERS service and projected SS of $2,400/month at 62, the FERS Supplement pays approximately $2,400/month from age 60 to 62. After 62, regular Social Security replaces the supplement (you have to actually claim SS for it to start; otherwise the supplement just ends).

The supplement makes early retirement viable for federal employees with sufficient years. It bridges the gap between federal retirement at MRA+30 and SS eligibility at 62.

Important: the supplement is subject to earnings test like regular Social Security. If you earn over the SSA threshold ($23,400 in 2026), your supplement is reduced $1 for every $2 over the limit. If you plan post-federal employment in a high-earning role, the supplement may be partially offset.

FERS + Military Retirement — The Double-Stack

For military retirees who transition to federal civilian employment, you can collect both retirements:

- Military retired pay (continues from active military retirement)

- FERS pension (based on civilian federal service)

- Two pensions, two different formulas

You cannot buy back the years you already used for military retirement (would be double-dipping). But any military service AFTER your military retirement (rare) or military service that didn’t produce a 20-year retirement can be bought back for FERS.

Plus VA disability compensation continues separately. Plus Social Security at age 62-70 based on combined work history.

For a military retiree who serves 22 years federal civilian after a 20-year military retirement, the total retirement stack at 65 might look like:

- Military pension (COLA-adjusted from military retirement)

- VA disability (rating-based)

- FERS pension (22 years × 1.0% × high-3)

- TSP withdrawals (combined from military and federal contributions)

- Social Security at FRA

This is the upper end of federal retirement income — five income streams, mostly inflation-protected. Worth planning toward.

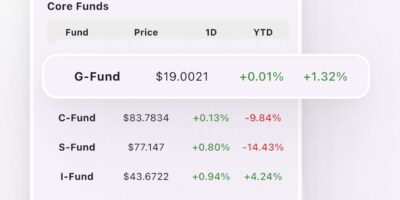

TSP — Same Funds, Federal Match

Federal employees have the same TSP options as military service members under BRS:

- 1% automatic agency contribution

- Match up to 4% (full 5% government if you contribute 5%)

- Same G, F, C, S, I, and L funds

- Same contribution limits ($23,500 in 2026 + $7,500 catch-up at 50+)

For federal employees coming from BRS military service, your TSP account moves seamlessly. Contributions continue, agency match continues, allocation continues.

The allocation discussion is the same as for military — most federal employees with long careers ahead of them should be predominantly in equity funds (C, S, I) rather than G. The G-fund trap costs federal employees just as much as it costs military service members.

The Decision Points Specific to Military-to-Federal

For someone transitioning from military to federal civilian work:

1. Within 2 years of federal start, complete military buyback. The deposit calculation is fixed for 2 years post-start. After 2 years, interest accrues, raising the cost. The buyback is almost always positive-ROI; do it early.

2. Don’t waive military retirement to buy back to FERS. Generally a bad trade. Keep military pension separate.

3. Plan for the FERS Supplement if retiring before 62. Know the earnings limit and how post-federal work affects the supplement.

4. Maximize TSP from day one of federal employment. The match is too valuable to leave on the table. 5% minimum.

5. Consider VA disability impact on FERS. VA disability doesn’t offset FERS pension. They stack independently.

What to Do This Quarter

For federal employees considering military buyback:

1. Request your military service deposit estimate. Through your federal HR or directly through FERSEP / OPM Form RI 90-1. Free, gives you the exact cost.

2. Compare cost vs lifetime benefit. Use the calculator to project pension with and without buyback. The ROI is almost always positive for active-duty time that didn’t produce a military retirement.

3. Pay the deposit if positive-ROI. Lump sum or payroll-deduction installments.

For federal employees evaluating MRA decision:

1. Run scenarios at MRA+30, MRA+20 reduced, and age 62 with 5+ years. Each has different annuity and supplement implications.

2. Factor the 1.1% multiplier bonus at age 62. Often worth pushing to 62 if you have 20+ years.

3. Plan post-retirement earnings carefully. If retiring before 62, the FERS Supplement earnings limit constrains what you can earn from civilian work.

Stay in the loop

Get the latest dod retire.com updates delivered to your inbox.